Why is Financial Planning for Retirement Critically Important in 2026?

Financial planning for retirement is critically important in 2026. According to the American Psychiatric Association, over 72% of U.S. adults report feeling stressed about money—and retirement uncertainty sits at the heart of that anxiety.

Economists believe 2026 will be a pivotal year for American pocketbooks. Recent geopolitical tensions involving Venezuela and Ukraine have pushed stock market volatility to unprecedented levels. Yet retirement planning remains a marathon, not a sprint. A well-structured retirement financial planning strategy helps you weather short-term turbulence while building long-term security.

The benefits of thoughtful retirement planning extend beyond numbers: financial security, independence, and peace of mind. Consider this—roughly 70% of people turning 65 will need some form of long-term care during their remaining years. Without a plan, these costs can devastate retirement savings.

In this guide, we explore why is financial planning for retirement critically important, the key components of an effective plan, and actionable steps you can take today.

Why Planning Early Is Crucial

The benefits of early retirement planning compound over time—quite literally. When you start early, your money has decades to grow through compound interest. A 25-year-old investing $300 monthly will accumulate significantly more than a 35-year-old investing $500 monthly, despite contributing less overall.

Changing demographics and longevity add urgency to retirement planning. According to MoneyGuide, a 65-year-old married woman today has a 50% chance of living to age 90. Longer lifespans mean your savings must stretch further—and inflation erodes purchasing power every year you delay.

The risks of delaying are real. Many people assume they can work indefinitely, but health issues, industry changes, or caregiving responsibilities often force earlier-than-expected retirement. Those without adequate savings face difficult choices: reduced lifestyles, dependence on family, or returning to work during their golden years.

Consider two hypothetical individuals. Sarah began contributing to her 401(k) at 25. Mike waited until 40, assuming he had time. At 65, Sarah enjoys financial independence while Mike scrambles to catch up—a common scenario that underscores key reasons to start retirement planning as early as possible.

Key Components of Financial Planning for Retirement

Understanding how to plan for retirement financially starts with mastering three core components: budgeting, investing, and risk management. Each plays a distinct role in building a secure future.

Budgeting and Expense Management

Effective budgeting forms the foundation of any retirement plan. Start by evaluating your current expenses—housing, transportation, food, and entertainment. Then project how these costs will evolve in retirement.

Healthcare deserves special attention. Medicare premiums, prescriptions, and out-of-pocket costs add up quickly. The average retired couple may need $300,000+ for healthcare expenses alone. Tracking these costs now helps you build a realistic savings target.

Housing decisions also impact your budget. Will you downsize? Relocate to a lower-cost area? Planning ahead gives you flexibility to make choices that align with your desired lifestyle.

Investment Strategies

Financial strategies for retirement involve selecting the right accounts and balancing risk appropriately. Common retirement vehicles include:

- 401(k) plans: Employer-sponsored accounts, often with matching contributions—essentially free money for your future

- Traditional IRAs: Tax-deferred growth with potential deductions on contributions

- Roth IRAs: After-tax contributions with tax-free withdrawals in retirement

Balancing risk and return depends on your age and timeline. Younger investors can tolerate more volatility through stock-heavy portfolios. As retirement approaches, shifting toward bonds and stable assets protects accumulated savings from market downturns.

Risk Management and Insurance

Insurance serves as a safety net, protecting your retirement savings from unexpected events. A comprehensive risk management strategy includes:

- Health insurance: Coverage for medical expenses, including Medicare supplemental plans

- Long-term care insurance: Covers assisted living or nursing home costs that Medicare doesn’t fully address

- Life insurance: Provides for dependents and can supplement retirement income through accumulated cash value

Without proper insurance, a single health crisis could drain years of savings. Evaluating your coverage now, and adjusting as needs evolve, keeps your retirement plan on track.

Benefits of Financial Planning for Retirement

Why is financial planning for retirement critically important? Because the benefits extend into every aspect of your future life. You’ve worked hard your entire life for this special season. The right financial plan can make our break your retirement.

Financial security and peace of mind top the list. Knowing you have sufficient savings eliminates the constant worry about making ends meet. You can focus on enjoying life with your spouse and grandkids rather than stressing over money and how you will make ends meet.

Achievement of long-term goals becomes possible with proper planning. For some retirees, this might be a trip to Europe, for others it could be paying for your grandchildren’s private education. We all have dreams. Regardless of what yours are, financial planning for retirement will help put you in the best position to achieve them.

Reduced stress from unforeseen circumstances provides emotional relief. Market corrections, health issues, or family emergencies become manageable when you’ve built contingencies into your plan. Planning doesn’t eliminate surprises but it can elimiante the stress that would otherwise come from them.

Common Mistakes to Avoid

You don’t know what you don’t know and even well-intentioned planners stumble. Recognizing these common pitfalls helps you sidestep costly mistakes.

Waiting too long to start ranks as the most damaging mistake. Every year of delay costs you compound growth. Starting at 35 instead of 25 could mean retiring with half the savings—even with higher monthly contributions.

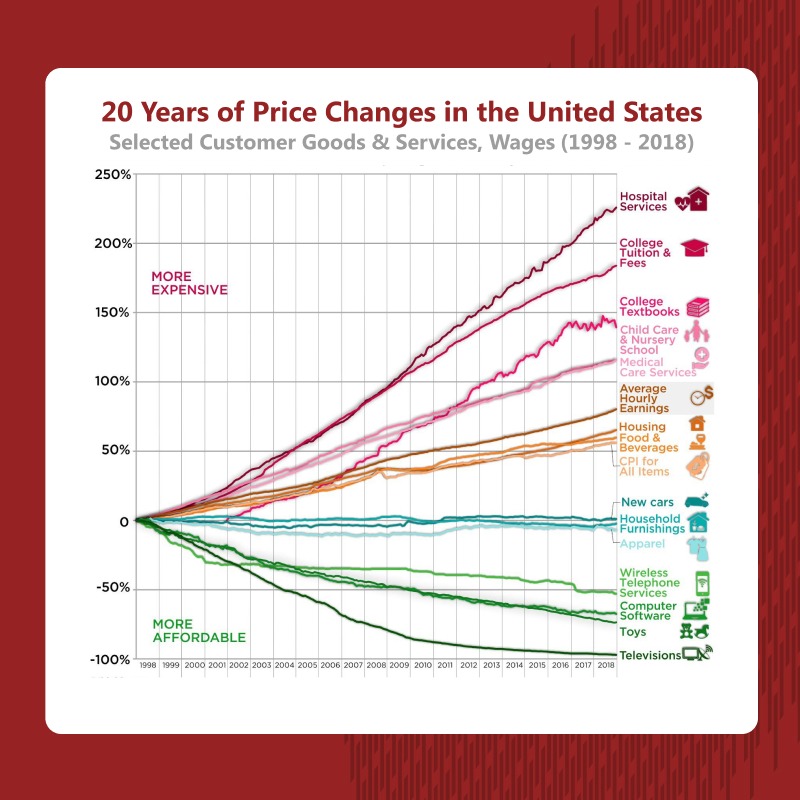

Underestimating inflation and healthcare costs leads to savings shortfalls. What costs $50,000 today may cost $100,000 in 20 years. Healthcare expenses, in particular, rise faster than general inflation. Build these realities into your projections.

CPI and other price indices – Bureau of Labor Statistics – https://data.bls.gov/PDQWeb/cu

Average hourly earnings – Bureau of Labor Statistics – https://data.bls.gov/timeseries/CES0500000008

Ignoring tax implications erodes your nest egg unnecessarily. Understanding the tax treatment of different accounts—traditional vs. Roth, taxable vs. tax-deferred—helps you optimize withdrawals and minimize your tax burden.

Failing to diversify investments concentrates risk. Spreading assets across stocks, bonds, and other vehicles protects against sector-specific downturns. No single investment should make or break your retirement.

How to Begin Your Retirement Journey

Starting your retirement financial planning journey doesn’t require perfection but it does require action. Here’s a practical roadmap:

1. Evaluate your current financial situation. Calculate your net worth by listing assets and debts. Review income sources, monthly expenses, and existing savings. This snapshot reveals your starting point.

2. Set short-term and long-term goals. Short-term: Build an emergency fund. Pay down high-interest debt. Long-term: Define your desired retirement age, lifestyle, and income needs. Specific goals create measurable targets.

3. Start small and automate. Even modest contributions matter when compounded over decades. Automating transfers to retirement accounts removes the temptation to skip contributions. Increase your rate as income grows.

4. Review and adjust regularly. Life changes—marriages, children, career shifts—require plan adjustments. Schedule annual reviews to ensure your strategy remains aligned with evolving circumstances and goals.

Take Action Today

The importance of starting early cannot be overstated. Time amplifies every dollar you save, turning modest contributions into substantial retirement funds. Waiting costs you this powerful advantage.

Creating a personalized retirement plan transforms abstract worries into concrete actions. Whether you’re 25 or 55, the best time to plan is now. For a deeper look at building a long-term strategy, explore our retirement planning guide here. If you need help preparing for your future, please reach out to a qualified financial advisor here at Guardian Resources. We can help you assess your situation, identify gaps, and build a strategy tailored to your unique circumstances.

Frequently Asked Questions

What is financial planning for retirement?

Financial planning for retirement is the process of setting goals and creating strategies to ensure financial security after leaving the workforce. It encompasses saving, investing, budgeting, tax planning, and risk management—all coordinated to support your desired lifestyle throughout retirement.

Why is it important to start retirement planning early?

Early planning maximizes compound growth—the exponential effect of earning returns on previous returns. Starting at 25 versus 35 can double your retirement savings, even with lower monthly contributions. Early action also provides flexibility to recover from market downturns and adjust strategies as life evolves.

What are the key components of a retirement plan?

A comprehensive retirement plan includes budgeting and expense projection, investment strategies across appropriate accounts (401(k), IRAs), risk management through insurance, tax optimization, and estate planning. These components work together to build, protect, and efficiently distribute your retirement wealth.

How much should I save for retirement?

A common guideline suggests targeting 70-80% of your pre-retirement income annually. However, individual needs vary based on desired lifestyle, healthcare requirements, and longevity expectations. Online calculators can help estimate your specific target, accounting for inflation, Social Security benefits, and investment returns.

Can financial planning for retirement reduce stress?

Absolutely. Research shows that individuals with retirement plans report significantly less financial anxiety. Planning provides clarity, control, and confidence. Instead of worrying about the unknown, you operate with a roadmap—knowing where you stand and what steps to take next. This peace of mind represents one of the most valuable benefits of early retirement planning.

Note: Individual needs vary. This information is general in nature and not intended as personalized advice. Please consult a qualified financial advisor for guidance tailored to your specific situation. Tax benefits vary based on individual income, filing status, and investment choices. Consult a tax professional for personalized guidance