")

The right tax planning strategies could be the difference between a disappointing return and a rewarding one. Few things are more complicated than the US tax code. However, obtaining a fundamental understanding of the basics can help you significantly reduce your tax liability when you submit your return.

I’ve seen too many people leave money on the table simply because they didn’t know their options. That’s what this comprehensive guide to tax planning is all about: giving you the tools to make smarter decisions with your money.

What Is Tax Planning and Why Does It Matter?

Tax planning, at its core, is the analysis and arrangement of your financial situation to maximize tax breaks and minimize tax liabilities. The purpose of tax planning strategies isn’t to cheat the system. Rather, it’s about using the tools the system offers. And there are lots of them.

The benefits go beyond just saving money during tax season. Effective tax planning helps you optimize your investments, stay compliant with tax law, and build long-term wealth. Think of it as financial hygiene. You don’t wait until you have a cavity to start brushing your teeth, and you shouldn’t wait until April to start thinking about your taxes.

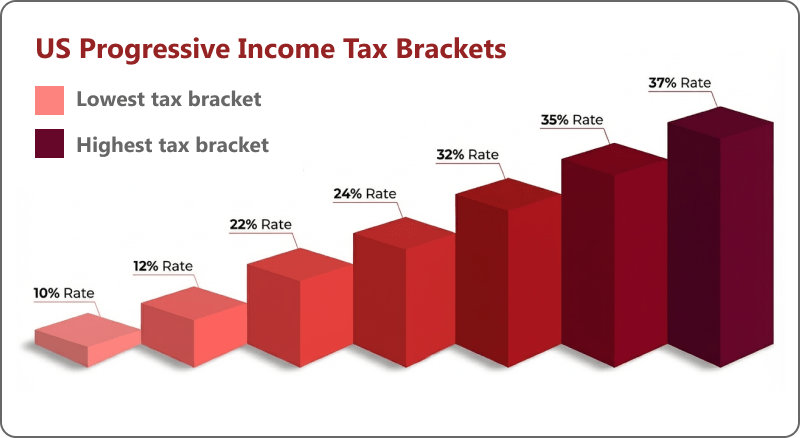

To plan effectively for the future, you must first understand your current tax situation, including which tax brackets apply to your present financial position. The United States has a progressive tax system with seven federal income tax brackets: 10%, 12%, 22%, 24%, 32%, 35%, and 37% (Tax Foundation, 2025).

In a progressive tax system, there are income thresholds for each incremental tax increase. Think of these “income thresholds” like buckets. Once the first bucket is filled, the remaining money spills over to the second bucket, and so on. The IRS then charges a tax rate for each bucket. Your first bucket will be charged 10%, your second 12%, third 22% and so on.

This system is called “progressive” because it increases the more money an individual earns. This is a critical concept to understand, as it forms the backbone of what we are trying to avoid—higher taxes that come from higher income levels.

Here’s another example to further explain this concept:

A single filer with $50,000 in taxable income. Your position in the 22% bracket for 2025 becomes clear. You need to pay 22% of the entire $50,000. No. You pay only 10% on the first $11,925, 12% on the amount between $11,926 and $48,475, and 22% on just the remaining amount. Individual tax planning needs a basic understanding of essential tax regulations to function properly.

Key Tax Planning Strategies

Maximize Retirement Account Contributions

Your employer might offer a 401(k) plan that gives you a tax break on money you set aside for retirement. The IRS does not require taxation for funds that you transfer directly from your paycheck into a standard 401(k) account. In 2025, you can funnel up to $23,500 per year into a retirement account. The contribution limit for people aged 50 and above reaches $31,000. The Secure 2.0 Act enables people aged 60 to 63 to make contributions of up to $34,750.

If your employer matches some or all of your contribution, you’ll get free money to boot.

Outside of employer-sponsored 401(k) plans, individual retirement accounts are your main alternative. With a traditional IRA, your contributions may be tax-deductible—how much you can deduct depends on whether you or your spouse is covered by a retirement plan at work and how much you make. The tradeoff? You pay taxes when you take distributions in retirement.

The Roth IRA operates through its own system, enabling you to withdraw funds tax-free in retirement while your initial contributions remain tax-free. The current tax payment is an advance payment that helps you avoid paying additional taxes in the future. Which one makes sense depends on your situation.

Utilize Tax Deductions and Credits

When it comes to lowering your tax bill, deductions and credits are your biggest allies. They both help you save, just in different ways.

Tax deductions allow you to subtract certain expenses from your taxable income, lowering the portion of your income that is taxed. Tax credits offer superior benefits because they let you subtract particular amounts from your total tax bill. A $1,000 tax credit reduces your taxes by exactly $1,000. Whereas a $1,000 tax deduction would decrease your taxes by $300 (assuming you are in a 30% tax bracket).

Common deductions include mortgage interest, property taxes, charitable contributions, and certain medical expenses that exceed set limits. Choosing to itemize your deductions makes sense when their total exceeds the standard deduction, which is $15,750 for single filers in 2025 and $31,500 for married couples filing jointly.

Beyond deductions, tax credits offer some of the most powerful savings opportunities available. Credits such as the Child Tax Credit, Earned Income Tax Credit, American Opportunity Credit, and residential energy credits can significantly reduce what you owe and, in some cases, increase your refund.

Income Timing and Capital Gains Strategies

When you receive income, it plays an important role in how much tax you pay. Deferring income can reduce your taxes if you expect your tax bracket to drop next year, whereas taking income now may be better if you expect tax rates to rise.

In addition to managing when income is recognized, investors can also reduce their tax burden by strategically managing how investment losses are handled. Under current U.S. tax law for the 2025 tax year, tax-loss harvesting allows investors to sell investments at a loss to offset capital gains and to deduct up to $3,000 of net capital losses per year against ordinary income, with any remaining losses carried forward to future tax years.

Tax Planning Tips for Beginners

There is a lot that can go into creating an effective tax planning strategy. If you are just getting started, focus on the basics. Here’s a list of steps to take if you are a beginner eager to save money next April.

Organize Financial Records

It might be a hassle at the start, but being organized will pay dividends in the long term (literally). It’s important that you keep all your tax documents and supporting documents, as they will help you during an audit. The IRS typically has three years to decide whether to audit your return, so keep your records for at least that long.

The law requires you to maintain records for specific situations, including six years for underreporting income by more than 25% and seven years for writing off a worthless security, and there is no time limit for cases where you failed to file a return.

Seek Professional Advice

A tax professional who understands your situation can identify opportunities that you would not discover through your own efforts. Most tax-savings strategies are underutilized because they apply only in very specific scenarios.

Tax software, together with a qualified tax professional, will help you identify your eligible deductions and determine if their combined value exceeds the standard deduction threshold.

Tax Planning for Different Income Groups

Salaried Individuals

By updating your W-4 form, you can better align your tax withholding with your actual tax situation. Increasing your withholding is wise if you faced a large tax bill last year, while reducing it may make sense if you received a sizable refund, allowing you to use that money more effectively throughout the year.

In addition, try to maximize your retirement savings through all available options. Use FSAs and HSAs when your employer provides them, and claim all eligible state and local tax deductions.

Business Owners

Self-employed individuals can establish their own 401(k) retirement plans. You can also deduct legitimate business expenses, home office costs, and health insurance premiums. Unlike employees, self-employed individuals must make quarterly estimated tax payments to avoid underpayment penalties.

Investors

You should use tax-loss harvesting as one of your investment strategies. Long-term capital gains (assets held more than a year) are taxed at lower rates than short-term gains. A donor-advised fund provides donors with an effective way to combine their charitable donations into a single large contribution, which they can use to maximize their tax benefits during their most profitable years.

For education savings, 529 plans let you save for college with potential state tax deductions. The 2025 gift tax rules will impose penalties on donors who make gifts of more than $19,000 to each beneficiary.

Common Mistakes to Avoid

Procrastination stands as the number one issue. Year-end tax planning is significantly more effective than scrambling in April. You must wait until you can contribute to your account, adjust your withholding amounts, and take advantage of loss harvesting before the deadline arrives.

Missing deadlines is another killer. The tax deadline gives you an opportunity to fund your IRA for the previous year, so you should use this chance.

Benefits of Effective Tax Planning

Your ability to understand federal income tax operations, combined with the strategic application of this knowledge, will help you achieve maximum financial savings while minimizing your financial burden and enhancing your economic security. You’re not leaving money on the table. You’re not scrambling at the last minute. You’re in control.

Tools and Resources for Tax Planning

Online Calculators and Apps

Modern tax software helps users estimate their tax obligations, explore different deduction strategies, and see the financial impact of various decisions, all while providing easy access to available tax credits. These tools have become remarkably sophisticated and user-friendly.

Professional Tax Advisors

A professional advisor delivers value to clients who need help with complex financial situations, which include high-income earners who must deal with AMT rules and business owners who receive income from various sources.

Take Action Today

Tax planning requires ongoing effort because it must be done throughout the year. The system generates increasing effects that expand in magnitude during each successive year. Your first step should be to start your development process from your present work position. Track your expenses. Understand your brackets. Max out what you can.

You can begin using these tax planning methods at present to achieve improved financial savings while reducing your future tax responsibilities. Your future self will thank you.

")